Building Financial Stability With a Low Income Savings Challenge

Managing money on a limited income often feels like an exercise in frustration. Traditional savings advice—set aside 20% of each paycheck, build a six-month emergency fund—can seem disconnected from the reality of covering rent, groceries, and utilities with little left over. The Low Income Savings Challenge reframes the entire approach, turning small, consistent actions into measurable financial progress without requiring a dramatic lifestyle overhaul.

At its core, a savings challenge is a structured, time-bound commitment to set aside money according to a specific pattern or rule. What makes a low-income version distinct is the deliberate scaling of expectations. Instead of aiming for large lump sums, participants work with micro-amounts—sometimes as little as one dollar at a time—building momentum through repetition and visible tracking. This printable planner format adds a tactile, analog layer that keeps the process grounded and personal.

What the Low Income Savings Challenge Actually Involves

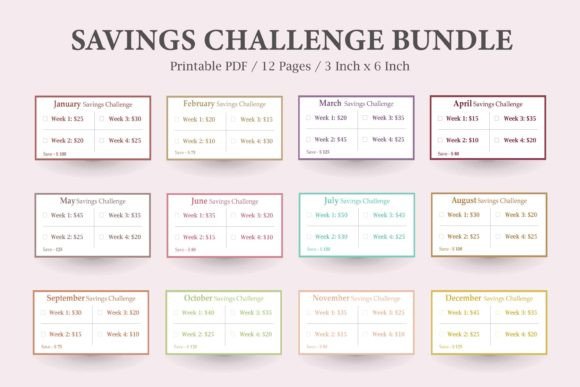

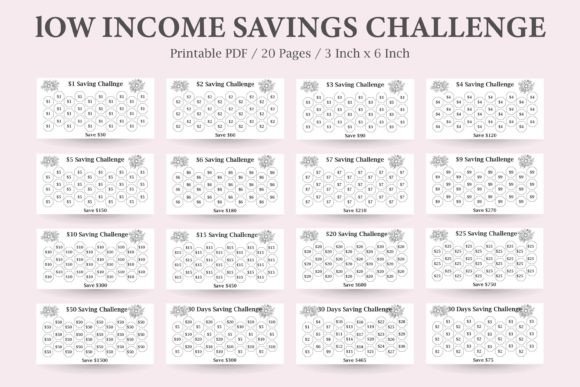

The challenge operates on a straightforward premise: you select a savings goal and follow a predetermined sequence of deposits over a set number of days or weeks. The A6 Low Income Savings Challenge Printable Planner bundles multiple challenge formats into a single 20-page resource, giving you the flexibility to match your current financial capacity. Options range from the USD 1 Savings Challenge—where each deposit is a single dollar—to more graduated approaches like the 2, 3, and 4 savings challenges that incrementally increase the amount saved over time.

Each challenge page functions as a tracker. You color in, check off, or initial a box each time you make a deposit. This visual feedback loop is where the psychology of the method takes hold. Watching a page fill up creates a sense of accomplishment that a digital bank balance rarely provides. The minimalist, ink-friendly design means you can print these sheets at home or at a library without worrying about excessive toner use, keeping the entire process affordable from the start.

Where a Savings Challenge Fits Into Your Broader Financial Process

The Low Income Savings Challenge isn’t a standalone fix—it works best when integrated into a larger money management routine. Think of it as the execution layer sitting beneath your budget. Your budget determines how much you can allocate and when; the challenge provides the structure and accountability to follow through.

Before starting, take a quick inventory of your monthly cash flow. Identify any recurring expenses that could be trimmed slightly to free up the small amounts needed for the challenge. This preparation phase matters because it turns abstract intentions into a concrete plan. You might decide to skip one takeout coffee per week, cancel an unused subscription, or redirect cash from a side gig directly into the challenge.

During the challenge period, the tracker becomes a daily touchpoint. Some people prefer morning check-ins, marking their deposit after reviewing their spending from the previous day. Others integrate it into a weekly budgeting session, making the deposit alongside other financial tasks like bill payments or expense tracking. The key is consistency—attaching the savings action to an existing habit reduces the mental effort required to maintain momentum.

Aligning Challenge Selection With Real-World Goals

Choosing the right challenge from the bundle depends on what you’re saving for and your current income rhythm. A 30-Day Savings Challenge works well for short-term targets like building a small emergency buffer or covering a known upcoming expense such as a car registration renewal or a medical copay. The compressed timeframe keeps motivation high and the finish line visible.

For longer-term objectives—saving for holiday expenses, building a security deposit, or creating a modest investment starter fund—the incremental challenges like the 1 through 4 savings trackers offer a gentler pace. You can complete one challenge and immediately start another, effectively layering multiple cycles to build a larger total over several months. This modular approach prevents burnout while steadily growing your savings habit.

Practical Implementation: Making the Challenge Stick

Printing the planner pages is step one. What happens next determines whether the challenge becomes a lasting tool or abandoned clutter. Here’s where the process-oriented approach pays off.

Start by selecting a physical home for your printed tracker. An A6 binder, a clip on the refrigerator, or a dedicated spot in a desk drawer all work. The visibility factor matters—place it somewhere you’ll encounter regularly without it becoming intrusive. Some participants tuck the tracker inside a budgeting notebook or planner they already use, merging the challenge into an existing organizational system.

Decide on your deposit method. Cash-based savers often use an envelope system, physically moving bills into a designated envelope each day. Digital-first users might transfer money to a separate savings account or a platform like a high-yield savings app. The method isn’t critical; consistency is. What matters is that each completed deposit gets recorded on the tracker immediately. Delaying this step breaks the feedback loop.

Handling Irregular Income and Unpredictable Weeks

Low-income households frequently deal with fluctuating pay schedules, seasonal work, or gig-based earnings. The Low Income Savings Challenge accommodates this reality when you approach it flexibly. If a tight week makes the planned deposit impossible, skip it without guilt and resume when cash flow improves. The tracker pages aren’t rigid contracts—they’re guides. Some challengers even customize their approach by shuffling deposit amounts across days, completing higher-value deposits during flush weeks and minimal ones during lean periods.

This adaptability distinguishes a printable challenge from automated savings apps that withdraw on fixed schedules regardless of your account balance. You retain full control over when and how much to save, which aligns better with the lived experience of budgeting on a variable income.

How the Savings Challenge Interacts With Other Financial Tools

The Low Income Savings Challenge Printable Planner doesn’t replace budgeting software, spreadsheets, or banking apps—it complements them. Many users pair the analog tracker with a digital budgeting tool like a simple spreadsheet or a free app. The digital side handles categorization and long-term tracking; the printed challenge handles motivation and daily accountability.

For those already using a zero-based budget or the envelope method, the challenge integrates seamlessly. Your budget tells you that you have, say, twenty dollars available for savings this month. The challenge structures exactly how those twenty dollars get set aside, removing the decision fatigue of figuring out savings amounts on the fly.

In relationships or households where finances are shared, a visible tracker creates transparency. Partners or family members can see progress in real time, which often encourages collective participation. A child watching a parent fill in savings boxes learns about goal-setting and delayed gratification indirectly, through observation rather than lecture.

Organization and Long-Term Consistency

Maintaining a savings rhythm over months requires more than initial enthusiasm. Organization prevents the tracker from becoming forgotten paper. Consider grouping your printed challenges by goal category: emergency fund pages together, specific purchase goals separate, seasonal savings in another section. Label each page clearly with the goal name and target completion date.

Review your progress during a weekly financial check-in. This doesn’t need to be lengthy—five to ten minutes spent reviewing what worked, what didn’t, and what adjustments the upcoming week needs. These micro-reviews catch problems early. If you’ve missed three deposit days in a row, that signals a need to either scale back the challenge intensity or address a spending leak elsewhere in your budget.

Efficiency Gains Through Batching and Planning

Batching reduces the administrative friction of the challenge. Instead of making a daily transfer, some savers calculate the week’s total deposits and move that amount in one transaction, then mark the daily boxes as each day passes. This approach works especially well for those paid weekly or biweekly. The key is to still engage with the tracker daily—the visual marking ritual matters more than the actual transfer timing.

Planning ahead for known financial disruptions—holiday weeks, back-to-school expenses, annual insurance payments—prevents the challenge from derailing. If you know December will be tight, start a more aggressive challenge in October or November to build a cushion, then scale back during the expensive month. The planner bundle’s variety of challenge formats makes this kind of strategic sequencing possible.

Quality Control: Avoiding Common Pitfalls

Even well-designed systems fail if underlying issues go unaddressed. One common mistake is choosing a challenge that’s too aggressive for your current reality. Saving three dollars per day sounds modest, but over 30 days that totals ninety dollars—a significant sum for someone whose disposable income is already stretched thin. Start conservatively. Completing a 1 Savings Challenge and feeling successful builds more long-term capability than abandoning an overly ambitious 4 challenge halfway through.

Another pitfall involves treating savings as whatever remains after spending. The challenge works precisely because it flips this order. You save first—even if the amount is tiny—and then spend from what remains. This mental shift, sustained over weeks and months, rewires financial habits more effectively than any single large deposit ever could.

Watch for the temptation to raid your savings for non-emergency purchases. If the money sits in a checking account, it’s psychologically available for spending. Moving challenge funds to a separate, slightly less accessible account adds a friction layer that protects your progress. Even a simple secondary savings account at the same bank, without a debit card attached, serves this purpose.

Extending the Challenge Beyond the Printed Page

Once you’ve completed a few cycles, the principles embedded in the Low Income Savings Challenge start influencing other financial behaviors. The daily attention to small amounts trains you to notice spending leaks—those three-dollar impulse purchases that previously went unexamined. The tracker’s visual proof that small deposits accumulate into meaningful totals makes the abstract concept of saving tangible and trustworthy.

Some participants graduate from the printable challenges to larger financial goals, using the same micro-action framework to fund retirement contributions, investment accounts, or education savings. The underlying process—choose a target, break it into tiny steps, track progress visually, adjust as needed—scales far beyond the initial challenge amounts.

The bundle format also supports concurrent challenges. You might run a 30-day challenge for an immediate goal while simultaneously working through a longer-term incremental tracker for a larger objective. Managing two trackers takes marginally more effort than one while doubling the savings impact and reinforcing the habit from multiple angles.

Integrating Savings Challenges Into Workflows and Routines

For freelancers, entrepreneurs, and gig workers, irregular income makes traditional automated savings difficult. The printable challenge approach offers a manual but reliable alternative. After receiving payment for a project or gig, you can front-load several days’ or weeks’ worth of challenge deposits while cash is available, then coast through leaner periods with the tracker still showing progress.

Educators, marketers, bloggers, and other professionals can adapt the challenge concept to business finances—saving for equipment upgrades, course enrollments, conference attendance, or tax obligations using the same small-step methodology. The A6 size of the printable planner makes it portable enough to slip into a work bag, backpack, or notebook cover, so the tracker travels with you throughout the day.

Small business owners managing tight margins find the challenge format useful for building a cash reserve without disrupting operational cash flow. The psychological benefit of seeing a dedicated business savings tracker fill up parallels the personal finance experience—momentum builds confidence, and confidence supports better financial decision-making across the board.

Ultimately, the Low Income Savings Challenge succeeds because it respects the reality of limited resources while refusing to treat that reality as a permanent barrier. The printable planner format costs little to acquire, almost nothing to use, and delivers returns measured not just in dollars saved but in the quiet confidence that comes from proving to yourself that you can build something from small, consistent actions—one filled-in box at a time.