Rethinking Personal Finance with a Savings Challenge and Savings Tracker

Money management often feels like a tug-of-war between immediate needs and distant goals. For many, the very idea of putting money aside can trigger anxiety, especially when income is tight. Yet shifting the lens from deprivation to small, intentional actions is what a Savings Challenge and a reliable Savings Tracker offer. They are not about grand austerity—they’re about rewriting your financial narrative one micro-step at a time. The Minimalist Low Income Savings Challenge Bundle transforms this philosophy into a tactile, month-by-month journey that respects your reality while nudging you toward meaningful progress.

Why Low-Income Budgeting Deserves a Different Kind of Toolkit

Conventional financial advice frequently assumes a baseline of disposable income that simply does not match the lived experience of freelancers juggling irregular paychecks, young professionals paying down student debt, or families navigating rising living costs. When every dollar is accounted for before it arrives, the suggestion to “save 20% of your income” can feel absurd. This is where the Low-Income Budgeting mindset becomes essential. It recognizes that saving isn’t about percentages—it’s about building the habit of consistency with amounts that feel doable rather than punishing.

Modern saving strategies are moving away from rigid, one-size-fits-all benchmarks. Users now gravitate toward customizable, visual systems that acknowledge financial diversity. A Budget-Friendly Savings Tracker that allows you to save $75 one month and $150 the next mirrors the reality of variable income. The Mini Savings Challenge Trackers embedded in this bundle cater precisely to this need, offering a gentle structure that flexes rather than breaks under pressure.

The Shift Toward Tangible Tracking in a Digital World

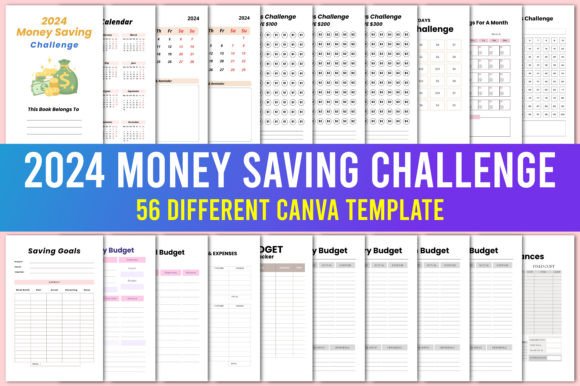

We live saturated in apps that promise to automate savings. Yet for many, the detachment of a screen is the very reason those methods fail. There’s a growing counter-movement embracing analog tools—planners, binders, and printable trackers—that demand physical engagement. Writing down a completed saving day, coloring a tiny icon, or slotting a tracker into an A6 budget binder creates a sensory feedback loop that digital notifications can't replicate. The Money-Saving Planner and Frugal Savings Tracker tap into this psychological ownership. When you physically mark your progress, you externalize a commitment, making it harder to ignore.

This is especially relevant for creators, educators, and entrepreneurs who spend hours online yet crave offline anchors for their personal goals. The portability of A6 mini challenges means your savings intention travels with you—tucked inside a cash envelope or a planner cover. It transforms a fleeting thought (“I should save more”) into a visible, daily prompt.

Debt Management and Emergency Funds: Small Sums, Significant Impact

One of the most pragmatic uses of a Savings Challenge Bundle is building a micro emergency fund while simultaneously tackling debt. Many low-income earners feel forced to choose between the two, but the monthly structure removes that false dilemma. January might encourage saving $100, while February dials it down to $75. These are not fixed mandates; they are invitations. Someone clearing high-interest debt could use the challenge to accumulate a modest buffer of $500 over several months, preventing a single car repair from sending them back to credit cards.

Observations from user behavior show that when a target is broken into labeled, time-bound chunks, the brain perceives it as a game rather than a chore. The Money Management Kit approach celebrates mini wins. Completing a March “Save $125” tracker reinforces the identity shift: you become someone who saves, regardless of the amount. That identity is far more protective than the cash itself, because it shapes future decisions around spending, side hustles, and financial conversations.

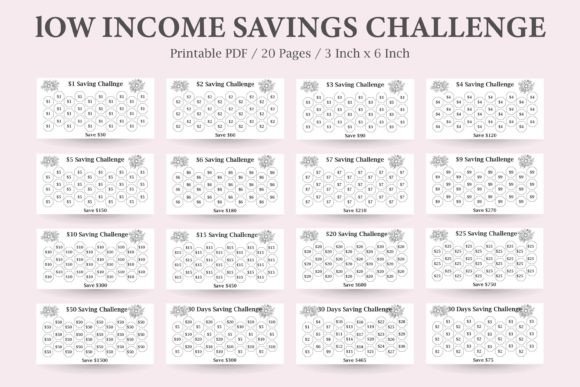

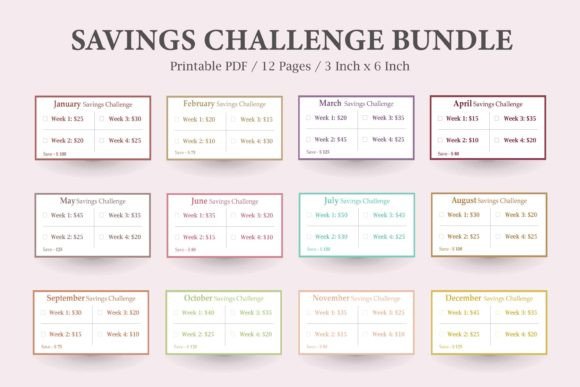

A Look Inside the Minimalist Low Income Savings Challenge Bundle

The power of this system lies in its deliberate sequencing. Rather than a flat monthly expectation, the bundle offers 12 distinct challenges that ebb and flow. This rhythm acknowledges that life is not linear. Below is the included monthly breakdown, which acts as both a roadmap and a gentle nudge:

- January: Save $100

- February: Save $75

- March: Save $125

- April: Save $80

- May: Save $125

- June: Save $80

- July: Save $150

Additional months continue this pattern, designed to accommodate seasonal fluctuations—higher saving goals during months when people often receive tax refunds or have fewer social obligations, and lighter goals during back-to-school or holiday periods. This isn't arbitrary; it’s a form of Economic Savings Goals setting that works with, not against, common financial cycles. Users can start in any month, reset as needed, or combine multiple trackers to target specific purchases, like a new laptop for a freelancer or holiday gifts without guilt.

How A6 Mini Savings Challenge Trackers Fit Into a Modern Money System

The format matters. The A6 size is intentionally compact, slipping into an Affordable Budget Planner or a ring-bound binder. For individuals using cash envelope budgeting—a method regaining popularity among those who want to curb card-based impulse spending—these trackers become immediate allies. Write a savings goal on the envelope, and tuck the matching tracker inside. Each time you divert cash into that envelope, you color in a segment. The physical accumulation feels weightier than a digital balance.

For content creators, marketing professionals, or small business owners, the bundle can also serve as an example of effective user experience design. It solves a pain point: people want to save but feel directionless. The themed trackers offer a start and an end point, reducing cognitive load. There’s no setup, no monthly recalculation. You print, you bind, you begin. This ease-of-use is what makes a Savings Planner Bundle appealing across generational lines, from digital natives exhausted by screen time to older adults who prefer paper-based clarity.

Redefining Frugality as Intentional Spending

Frugality often gets a bad name, mistakenly linked to deprivation. The shift in conversation now frames it as selective abundance. A Frugal Savings Tracker isn’t about skipping coffee; it’s about deciding that a trip next spring matters more than random online purchases. The tracker acts as a commitment device. When you see your July “Save $150” tracker partially filled, and an e-commerce sale tempts you, you’re faced with a concrete visual trade-off: finish the tracker or abandon it for a fleeting thrill. That moment of decision is where real money habits are forged.

This reframing is particularly useful for professionals working in education, non-profits, or creative fields where pay may be modest but aspirations are rich. The Low Income Savings Challenge philosophy replaces guilt with agency. You’re not “bad with money”; you just needed a structure that respects your context. Each completed challenge is a quiet statement that your financial capacity is growing, even if your salary isn’t yet at the level you hope for.

Practical Ways to Integrate the Bundle Into Daily Life

Adopting a new financial tool is only effective if it slips into existing routines. Here are grounded strategies observed among successful users:

1. Pair with a weekly finance ritual. Every Sunday evening, review the current month’s tracker. Transfer the designated amount—whether it’s $5 or $20—into a separate account or envelope. The ritual strengthens consistency without demanding daily attention.

2. Combine with a visual goal board. Place a photo of the goal (a vacation rental, a new skill course, a debt-free date) next to your binder. The Money-Saving Planner becomes not just a tool but part of a broader motivational environment.

3. Use the mini challenges as teaching tools. Educators and parents can introduce children to saving through these trackers, adapting the amounts. The act of coloring progress instills early positive money associations without complex concepts.

4. Leverage uneven income months. Freelancers and gig workers often experience a feast-or-famine cycle. During a high-income month, print two trackers—complete the current month and get ahead on a future one. This creates a visual buffer that reduces anxiety during slow periods.

5. Share progress selectively. In online communities focused on Economic Savings Goals, posting a filled tracker invites encouragement. The social reinforcement, done in safe spaces, can boost accountability without compromising privacy.

The Evolution of Savings Challenges in a Changing Economy

The renewed attention to printable savings tools does not exist in a vacuum. Rising inflation, gig economy prevalence, and a collective reevaluation of consumerism have all pushed people toward anti-fragile personal finance. An Affordable Budget Planner that costs a few dollars and can be reused indefinitely appeals to those tired of subscription-based budgeting apps that quietly drain their bank accounts. There’s also a growing desire for financial education that isn’t mired in jargon. The straightforward language of “Save $80 in April” cuts through the noise.

Interest in minimalism extends beyond aesthetics into financial simplicity. Consumers are curating their spending like they curate their homes—keeping only what adds true value. A Money Management Kit with clear, limited targets aligns perfectly with this mindset. You're not tracking every minuscule category; you’re focusing on one forward-moving action each month.

Moreover, the mental health dimension cannot be overstated. Money-related stress is pervasive. Having a Savings Tracker hung on a wall or slipped into a planner offers a daily reminder that you are progressing, even if slowly. It externalizes hope. For someone on a very restricted income, watching a January tracker fill up $10 at a time can shift their entire outlook from scarcity to incremental possibility.

Choosing the Right Savings Bundle for Your Journey

Not all savings bundles are created equal. Look for designs that prioritize clarity over clutter. The Minimalist Low Income Savings Challenge Bundle works because it strips away complexity—there is no confusing legend, no multi-currency abstraction. It answers the essential question: “How much do I need to put aside this month, and can I see myself doing it?” The inclusion of portable A6 formats indicates an understanding of real-life mobility, where budgeting often happens at kitchen tables and coffee shops, not just behind a desk.

For bloggers, content creators, and coaches who recommend resources to their audiences, bundles like these offer a tangible entry point. They bridge the gap between abstract advice (“build an emergency fund”) and executable steps. Recommending a Savings Challenge that breaks down a $1,000 annual goal into 12 varied monthly sprints makes the advice immediately applicable. It respects the reader’s intelligence while accommodating their limitations.

Ultimately, this bundle is a tool for designing your own financial momentum. Whether you use it to finally afford that certification course, gather a deposit for a better apartment, or simply prove to yourself that saving is possible on a small income, the trackers serve as both logbook and fuel. The conversation around money is changing—less about comparison, more about personal benchmarks. A Low Income Savings Challenge bundle puts the pen in your hand and whispers, “Start here, start now, with exactly what you have.”